狗仔卡

狗仔卡 发表于 2013-6-30 06:21 PM

发表于 2013-6-30 06:21 PM

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

If you follow Small-Caps, then you are probably aware of what just happened Friday and in the weeks leading up to the annual rebalancing of the Russell Indexes. For those not entirely familiar, I will explain the process and discuss an investment strategy that follows what is clearly "dumb money" selling out small-caps with no regard for valuation. With the market most likely still mired in a correction, fishing around for beaten up stocks is most likely a good use of time.

Russell Indexes: How They Work

Based in Tacoma, Washington, Russell Investments, owned by Northwestern Mutual Life, was founded in 1936. Many investors may be familiar with their role as the creator of the Russell Global Indexes, which have about $4 trillion in assets benchmarked to them according to the firm, but the company is also an asset manager, managing $152 billion.

When it comes to indexes, Standard & Poor's is the most popular provider for Large-Caps (S&P 500), while Russell wins for Small-Caps with its Russell 2000 index (IWM). You can see a complete list of their U.S. indexes here and click through to their global ones as well. A major difference between Russell and S&P is how the two organizations approach changes in the indexes. S&P has a committee that makes changes at various times, while Russell, for the most part (IPOs and corporate actions are the exceptions), makes an annual ranking and rebalances the index at the end of June (since 1989) in a process known as "reconstitution".

Here is a link to a presentation Russell has shared that explains the reconstitution process. The Russell 3000 consists of the top companies in terms of market cap that meet various criteria, with the top 1000 comprising the Russell 1000 and the next 2000 comprising the Russell 2000. This is obviously very important to passive investors, or those who try to just match the index (as opposed to active investors who try to outperform the index). Russell makes the changes based on market caps at the end of May and shares several updates with its clients. Here is the timeline:

(click to enlarge)

What Happens When Russell Reconstitutes?

There are four things that can happen to a stock in the reconstitution process:

- It can be outside of the R1000 or R2000 and be added

- It can be "promoted" from the R2000 to the R1000

- It can be "demoted" from the R1000 to the R2000

- It can be kicked out (deleted).

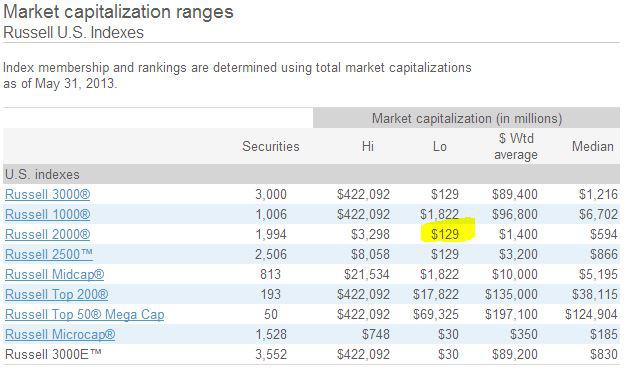

For 2013, the minimum market cap according to Russell for the R2000 is $129mm (based on 5/31):

(click to enlarge)

In 2012, the minimum was $101mm, so some stocks were likely deleted even if they appreciated over the past year.

Many traders begin anticipating new additions, and these stocks certainly benefit from the potential demand even before May ends. The bottom-line is that stocks added to any index get a one-time boost from index buyers and perhaps benefit from higher exposure, as active managers may be more prone to select from stocks within their benchmarks. For the most part, this game has been played already.

As far as promotions and demotions, I will reserve judgment, but my experience has been that the impact isn't substantial. What I want to address today is the deletions, which suffer from the exact opposite as the additions. Booted out by the index funds, these endure uninformed selling. Like the additions, this impact doesn't happen all at the last minute, as traders game the process.

Why Buy Russell Rejects?

There have been many studies over the years that explore the Russell reconstitution process. One study that I found interesting a few years ago titled "Long-Term Impact of Russell 2000 Index Rebalancing" (Cai & Houge) concluded:

Before I extol the simple and compelling logic, it's worth pointing out that the data was from 1989 to 2004. Things do change as market participants learn about excess returns, so there are no guarantees that what used to work yesterday will work today or tomorrow. With that said, this is simple mean-reversion. The Russell reconstitution forces the index investor to sell losers and buy winners, a "momentum" strategy. To me, this is kicking sand in someone's face. It's bad enough that the stock has declined, and then it faces an additional wave of selling due solely to passive investors essentially opening the door when the doorbell rings (on June 30th).

The strategy I am sharing, then, is value-oriented. Data supports it, as does logic. Unfortunately, it won't work for every single stock. There are dozens of deletions. A quantitative investor might just buy all of them, but that's not practical for most individuals. The takeaway that I would offer is that the deletions can be a source of potential ideas.

Let's Look at the 2013 Rejects

Russell has already published a complete list of additions and deletions to the Russell 3000. One of the deletions was from the R1000 and not due to market cap but rather other reasons. Excluding this, it appears that there were 88 R2000 deletions. I have an excel file with a lot of information that includes the complete list. From a summary perspective, the group of stocks had an average return last week of -0.5% compared to a 1.4% gain for the R2000 (24 declined by more than 5%). For June, the average loss was -3.6% compared to a -0.7% decline for the R2000 (27 fell more than 10%). YTD, these stocks have lost an average of 13.9% compared to a 15.1% gain for the R2000. Clearly, the pending deletions have impacted these stocks recently.

As I said, the complete list is available, but let's hone in a little:

- 30 of the names trade at Price/Tangible Book at 1X or less.

- 51 have more cash than debt

- 29 have positive YTD returns (not exactly losers)

- 26 have a trailing PE of less than 20X

To narrow the list and to give you a flavor of what we are talking about, I used Baseline to screen the 88 stocks:

- Positive trailing PE

- P/TB < 3

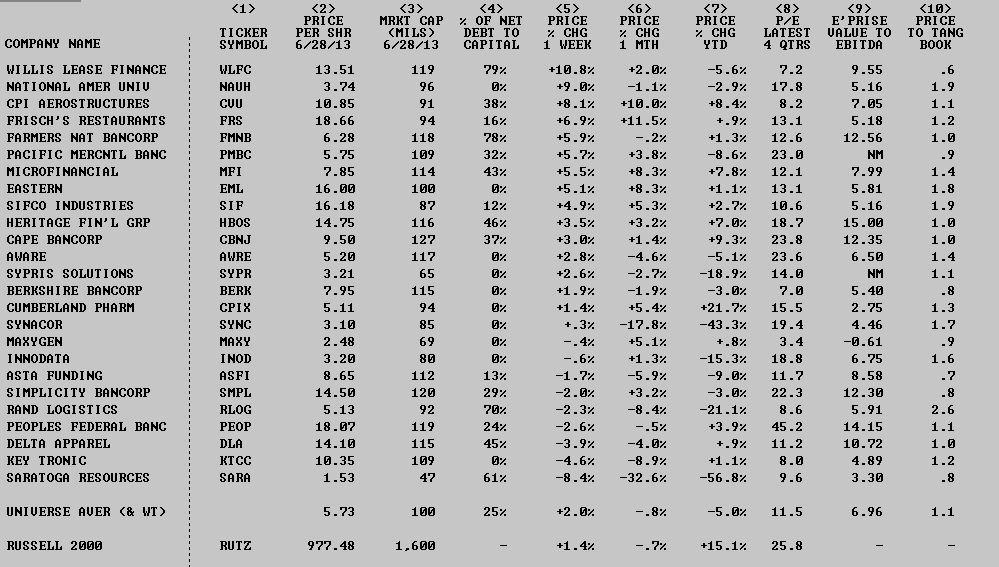

These are some potential babies in the proverbial bath, sorted by one-week-return (many were actually positive):

(click to enlarge)

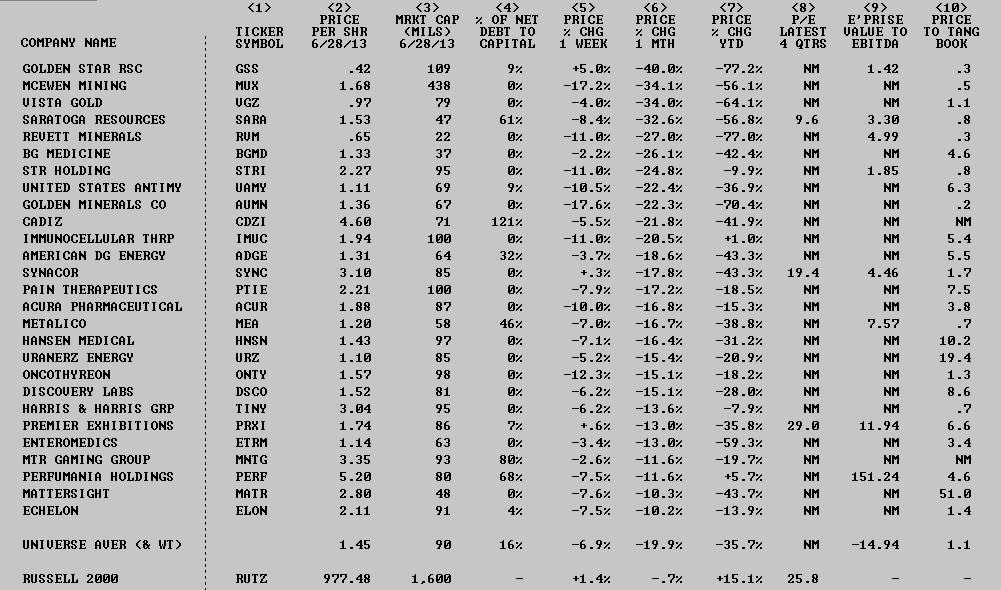

For all you bottom-feeders, here is the list of stocks that fell 10% or more in June:

(click to enlarge)

Buying Russell 2000 deletions is similar to an after-Christmas sale. You can get a great deal, but you are likely buying things that are out of favor. Many times losers keep on losing, and surely many of these companies that were rejected due to the market cap being insufficient will prove to be losers, but the research and logic suggest that index-based selling with no information content can provide positive returns to those who take the other side. It's a new quarter, and if you are looking for some ideas, the 88 deletions from the Russell 2000 might be a good starting point.

提升卡

提升卡 置顶卡

置顶卡 沉默卡

沉默卡 喧嚣卡

喧嚣卡 变色卡

变色卡