狗仔卡

狗仔卡 发表于 2013-6-25 01:59 PM

发表于 2013-6-25 01:59 PM

The Credit Services industry has been enjoying strong growth in recent periods in terms of net income. The top line growth has remained mature but the application of newer technologies have allowed to the companies to operate at better profit margins. The business model of credit services companies is extremely attractive as it allows for sustainable high profit margins. In this industry, some of the larger players are experiencing a stage of maturity. In order to pursue growth, these large companies have to look towards global expansion and technological advances to support their profitability. In this analysis, I aim to evaluate Visa Inc. (V) as a prospective investment opportunity as the company has shown remarkable returns to investors over the past years in terms of capital gains, dividends and stock repurchases. Along with addressing investor's considerations, the company has been able to produce decent financial performance by pursuing strategic expansions through international operations. In order to evaluate the potential of the company, a dividend discount model has been used in this analysis.

Industry Positioning, Business Strategy & Financial Performance

Visa is the largest player in the credit services industry with respect to market capitalization with a total value of $144.4 billion. Other major players include American Express (AXP) and MasterCard (MA). According to CSI markets data, the company holds a market share of 14.56%. In terms of market share, American Express is the largest player with a share of 32.56%. In this scenario, I expect Visa to maintain a significant degree of financial strength in order to hold its ground and pursue growth against larger competitors.

The strategy pursued by the company is different from the overall industry. The industry has continuously focused on its model's capacity to generate higher profit margins. On the other hand, Visa's profit margins have reduced over the recent periods. This is because the company has been adapting a long-term approach by focusing on increasing total volumes and improving its clientele.

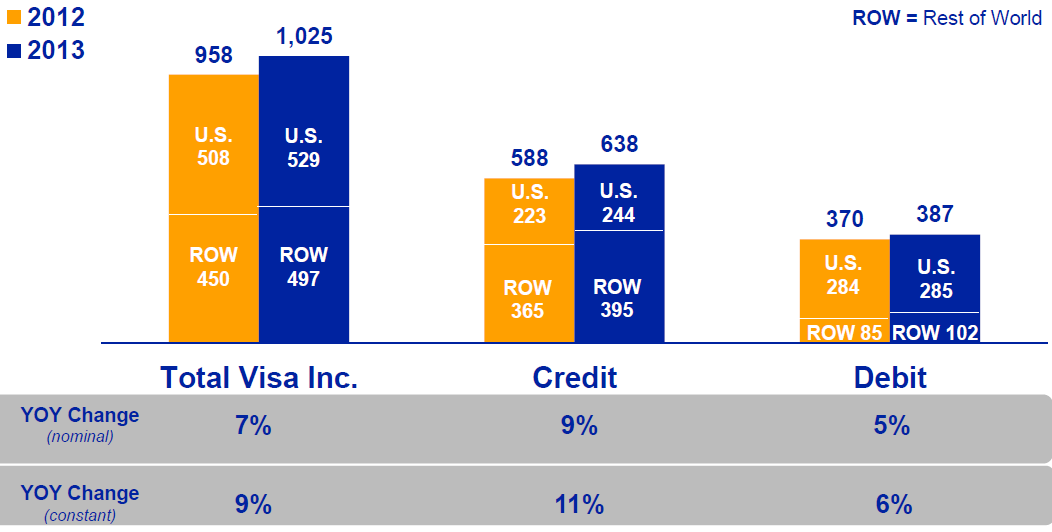

(click to enlarge)

Source: Earnings Presentation, FY13Q2

The above chart shows the payments volume of Visa in the second quarter of FY13 as compared to the corresponding volume of FY12. The chart firstly shows that a larger proportion of the volume is based on credit payments. Secondly, the overall activity of the business has increased in this quarter by 7%. The credit payments witnessed growth in the U.S. and in the rest of the world (ROW). On the other hand, debit services volume remained constant in the U.S. but showed a substantial growth of 20% in ROW.

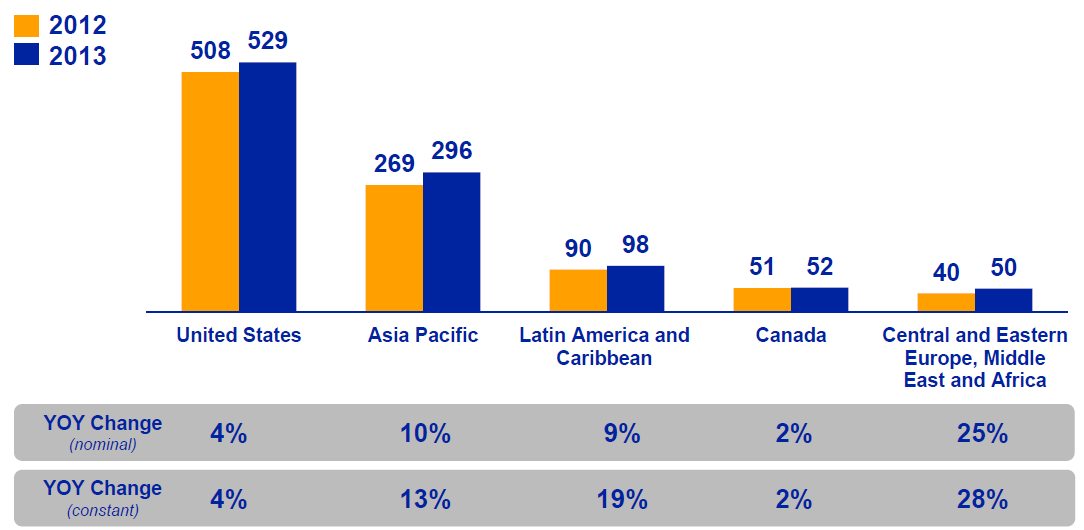

(click to enlarge)

Source: Earnings Presentation, FY13Q2

The above chart shows the geographical segmentation of the company's payments volumes. The chart shows that the company has a high exposure to the U.S. market (52% of total payments volume). At the same time, the operations in Asia Pacific, which currently contribute towards 29% of the total payments volume, have been growing at a much faster pace. This shows that the company is targeting the high growth regions in order to secure its future prospects.

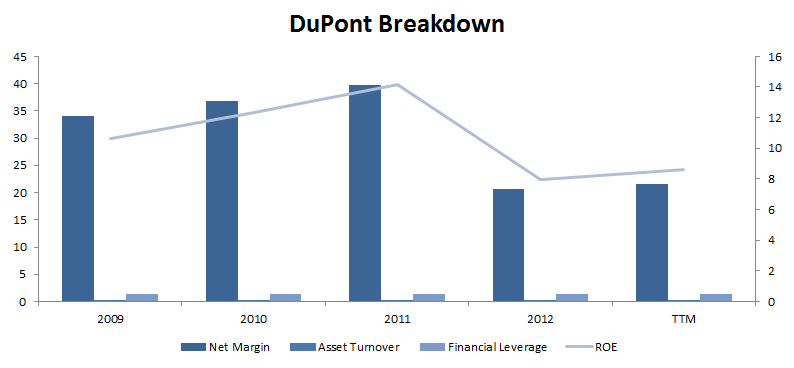

(click to enlarge)

Data Source: Morningstar

The above chart shows the DuPont breakdown of Visa's return on equity. The emphasis on increased volume through high-growth regions has resulted in a decrease in profit margins. This has translated into a lower return on equity in recent periods. More importantly, the chart shows that the company's return on equity is largely based upon its net margins instead of a high degree of financial leverage.

Valuation

The analysis of the company's performance suggests a decent upside potential. Therefore, a dividend discount model has been conducted in order to evaluate the extent of the company's potential.

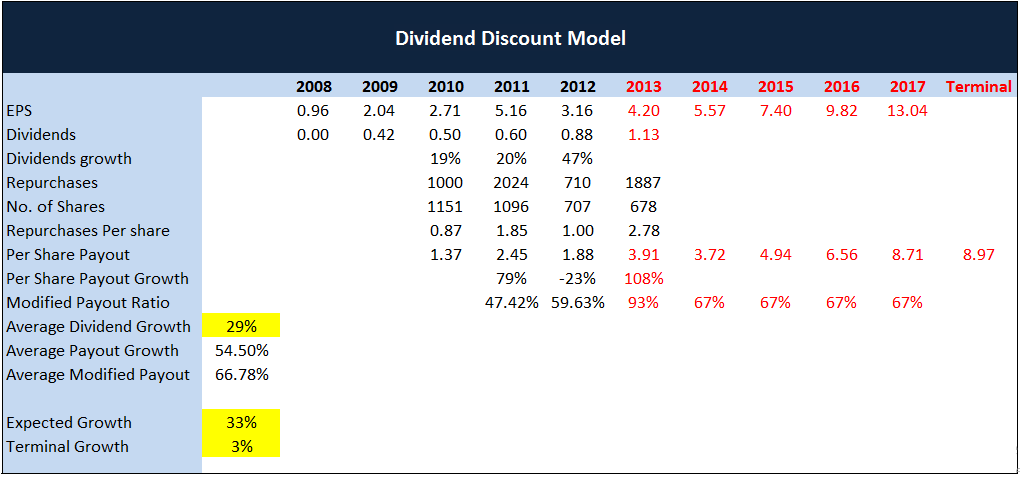

(click to enlarge)

Data Source: Morningstar

The above table shows the projections and assumptions of the dividend discount model. In this model, the average dividend growth rate of 29% has been used to calculate the dividends for FY13. The amount of repurchases has already been announced for the year, which has been incorporated as a direct input. Using these figures, a modified payout ratio has been calculated for FY13, which provided the trend over three years. The average for these three years was assumed to sustain for the next four years up until FY17. The two-stage model assumes that the company will be able to pursue its average growth due to its strong growth prospects in emerging markets like Asia. Therefore, an expected growth of 33% has been used. A terminal growth rate of 3% has been assumed.

(click to enlarge)

The above table shows the calculations for required rate of returns and a target price. The table shows that assuming a 6.67% required rate of return, the stock provides an upside potential of 9%.

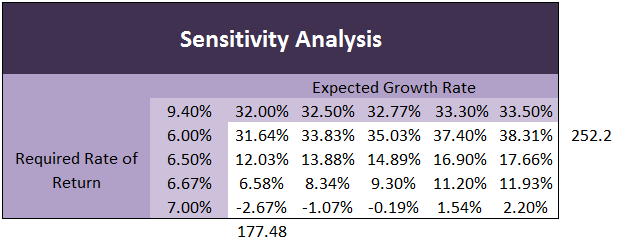

(click to enlarge)

The above table shows the sensitivity analysis, which has been conducted in order to account for different growth rates and required rates of returns. The best-case scenario shows an upside potential of 38.31%, which will occur at a stock price of $252.2. On the other hand, the worst case suggests a downside potential of 2.67%, which results in a target price of $177.48. The analysis shows that the stock offers a stronger upside potential.

Conclusion

The overall industry has been showing a lot of strength. Visa has recognized that in order to pursue further growth, the company has to compensate in terms of lower profit margins. This strategy is focused on gaining control of the growing sections of the global economy. The strategy is likely to yield impressive results and the valuation suggests a decent upside potential as well. Keeping these factors in consideration, I propose a buy stance for Visa.

提升卡

提升卡 置顶卡

置顶卡 沉默卡

沉默卡 喧嚣卡

喧嚣卡 变色卡

变色卡