狗仔卡

狗仔卡 发表于 2013-8-19 10:05 AM

发表于 2013-8-19 10:05 AM

I am a fairly fundamentals driven investor. I loved snatching up bank stocks Goldman Sachs (GS) at 0.9x book value, Bank of America (BAC) at 0.5x book value and Morgan Stanley (MS) at 0.7x book value in 2010 to 2012. While I am investing solely for the long-term (period of 5 years or longer), I pay close attention to short-term operational performance and catalysts that increase the odds of propelling a stock higher. I do have a strong concentration of bank stocks in my portfolio but I am willing to add to it if the underlying value proposition is tempting. Having said that, I believe that Citigroup (C) currently offers the most attractive risk-reward ratio of its peer group. The proposition is compelling on four counts: Citigroup operates a well-established banking franchise with an extensive emerging markets footprint, the business model is likely to be supported by macroeconomic tailwinds, its stock trades cheaply compared to fundamentals and its peers and it is the most beaten down stock of the respective peer group.

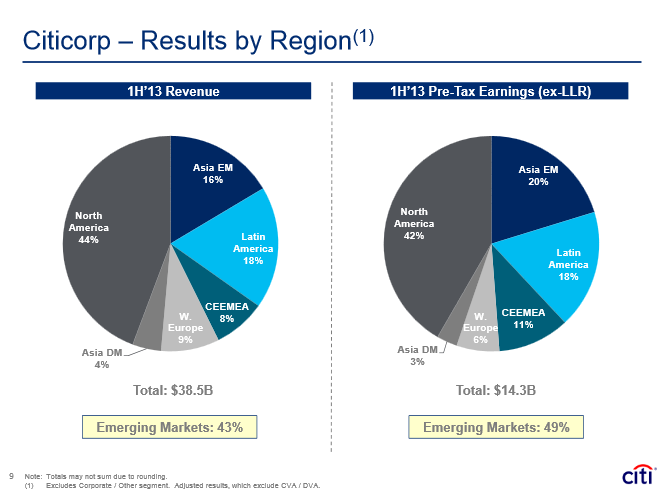

Citigroup relies on emerging markets to drive EBT

Citigroup derives significant amounts of revenue and cash flow from emerging markets. In 1H 2013 nearly half of revenues and EBT were generated outside the North American market. I think that, in the long-term, deposit- and loan-growth potential in Asia and Latin America are going to be much higher than in the saturated Western European and US markets. Having said that, I expect the importance of emerging markets to increase with larger amounts of earnings and cash flow generated overseas.

(click to enlarge)

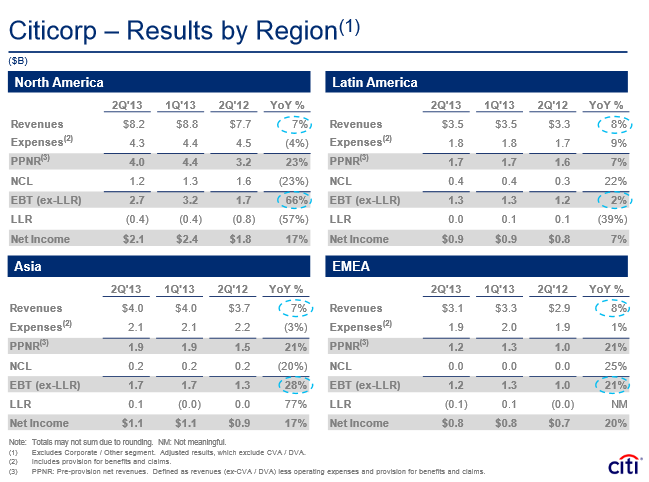

While y-o-y EBT growth rates in emerging markets are impressive and range from 2% in Latin America to 28% in Asia, it is delightful to see a meaningful improvement in EBT and net income growth in the North American market as well. I take this as confirmation that Citigroup is a fundamentally attractive international banking franchise with strong earnings potential.

(click to enlarge)

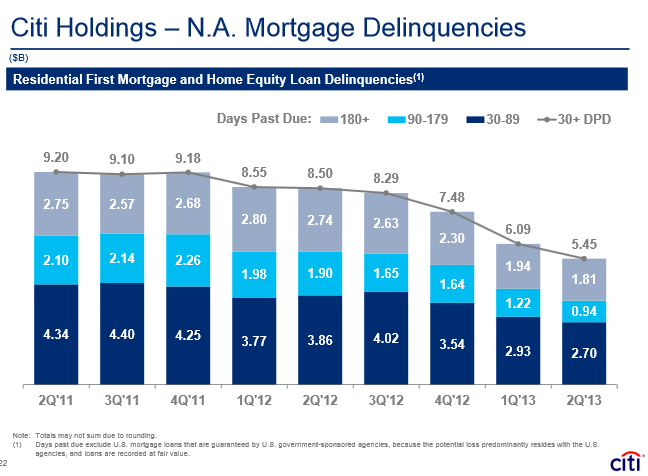

While the sudden spike in 2013 group profitability can principally be attributed to growth in ex-US international consumer banking and its securities & banking division, it is comforting that Citi Holding's mortgage delinquency trends, over which investors have fretted for years, are continuously improving (down over 40% since 2Q 2011) taken additional burden off of Citigroup's stock price (see below).

(click to enlarge)

Macroeconomic tailwinds

Investors need to realize that financial companies such as Citigroup react highly sensitively to changes in macroeconomic factors such as GPD growth rates and interest rates and are effectively a bet on global growth. Consequently, financials in general are inclined to perform extraordinarily poorly in contracting economies but have the potential to perform much better than the rest of the economy in expanding economies. Citigroup's recent 2Q 2013 results confirm that the industry outlook as improved and could possibly turbocharge EPS increases as US GDP continues to grow. Citigroup outperformed 2Q 2012: Citigroup revenues were up 8%, diluted EPS was up 25%, overall loan growth increased 4%, release of loan loss reserves stood at almost $800 million and its capital position increased with Basel III Tier 1 common capital ratio now at 10%.

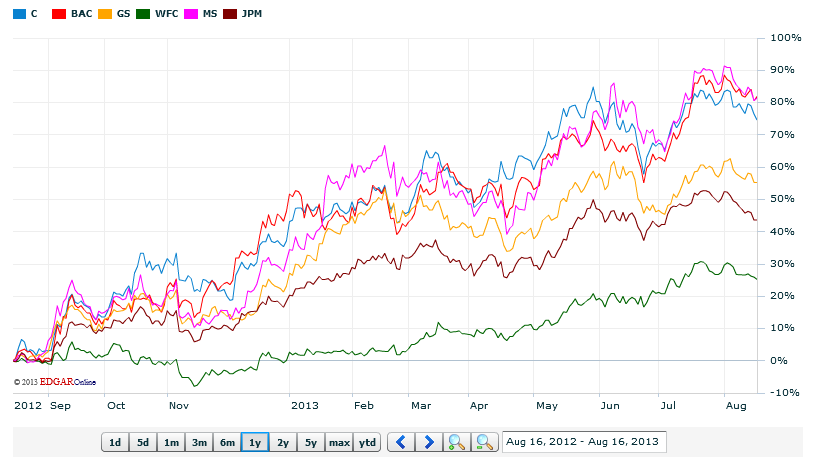

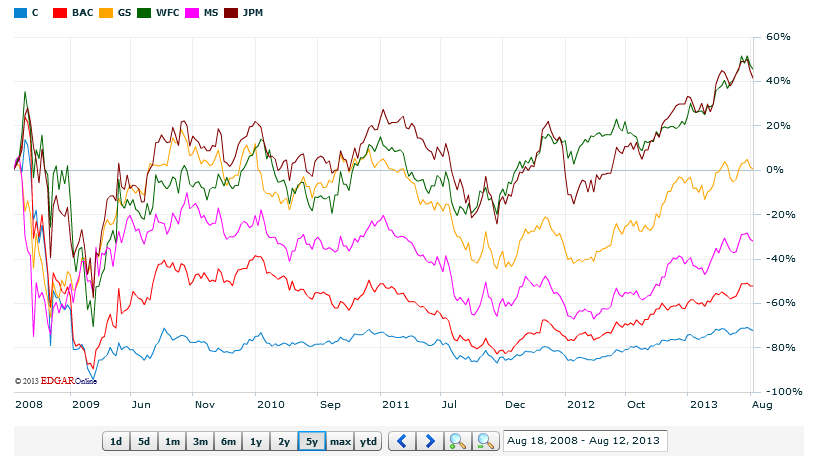

Beaten down like no other

Bank stocks have performed well as a group over the last 1-2 years and certainly have come a long way since the bottom in 2009. Since then financial companies have avoided burdening financial regulation that would have compressed EPS growth.

(click to enlarge)

I think it is very important for investors to understand that despite the recent run-up in stock prices for Citigroup and others, an isolated view of the last year does not tell the full story. Though Citigroup has outperformed Goldman Sachs and Wells Fargo (WFC) - both of them fetch a much larger valuation due to their premium to book value - Citigroup remains the most underperforming financial stock since the bottom of the stock market in early 2009.

(click to enlarge)

Citigroup is not only the worst performing banking franchise in terms of stock price development, but also remains one with the largest discount to intrinsic value. This allows investors who believe in the strength of its consumer franchise and a more accommodating industry environment to purchase the stock at still very attractive prices.

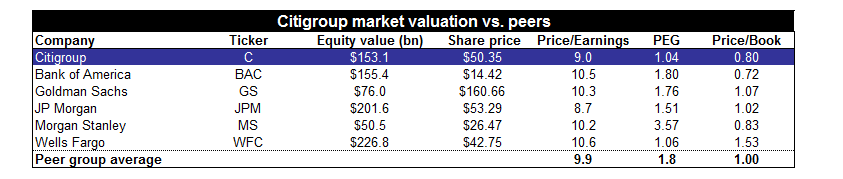

Market valuation and peer comparison

Citigroup currently trades at a forward earnings multiple of 9, the second lowest after JP Morgan (JPM) and below a peer group average of 9.9. From a book value perspective, Citigroup trades at a 20% discount to book value and peer average only being second to Bank of America which fetches a current book value discount of 28%. Citigroup's PEG ratio is the lowest of its peer group with 1.04.

(click to enlarge)

Conclusion

Citigroup operates a financially strong international banking franchise with growing EBT trends in all geographic areas of operation. The mix of revenues and earnings originating from overseas adds spice to Citigroup's stock. While being one of the worst performing financial stocks since 2009, I believe fundamentals and peer group comparisons regarding metrics such P/E, P/B and PEG justify a higher valuation.

Not taking into account multiple expansion and EPS growth, Citigroup is undervalued based on its discount to book value. However, I think that the entire financial sector still trades at a massive discount to its true earnings potential. Given the reasons outlined above, I believe that Citigroup can reasonably trade at a multiple of 13x 2014 earnings giving the stock 45% upside potential.

提升卡

提升卡 置顶卡

置顶卡 沉默卡

沉默卡 喧嚣卡

喧嚣卡 变色卡

变色卡