狗仔卡

狗仔卡 发表于 2013-6-28 06:12 PM

发表于 2013-6-28 06:12 PM

Despite a recent surge of more than 25% this year and over 50% in the past 12 months, Cisco (CSCO) still offers smart investors an excellent opportunity to invest in a long-term dividend growth stock at a very attractive price.

The stock has experienced an impressive rally, rising more than 100% since August 2011's lows of $13 to $25 in June 2013.

(Click to enlarge)

Interestingly, the company completely missed the broad rally lasting from January until the end of May, and caught up rather abruptly in mid-May after an impressive earnings beat. On the other hand, Cisco also stayed flat or even appreciated during the most recent S&P 500 (SPY) 4% slide. Because Cisco is less correlated to the broad market than some other stocks, holding part of your portfolio in Cisco may even bring the additional benefit of lower overall portfolio volatility.

(Click to enlarge)

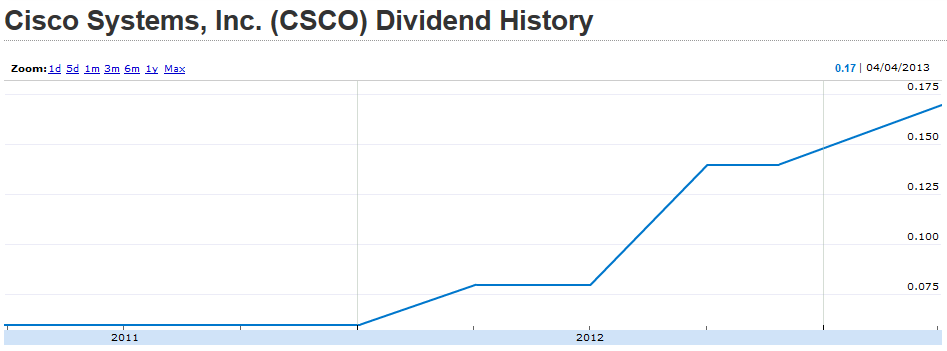

Dividend growth and sustainability

Since Cisco started paying out dividend in March 2011, the dividend has increased threefold in just two short years. And the uptrend is not stopping just yet.

(Click to enlarge)

The current dividend yield is 2.80%, still more than decent and more than the S&P 500 average. And Cisco is likely to keep growing its payout, albeit probably at a much slower rate.

What is even more important than the dividend growth rate or the current yield is dividend sustainability. In this respect, the company is in excellent financial shape, and investors are likely to be pleasantly surprised going forward.

The company has publicly expressed a commitment to keep paying out at least 50% of the free cash flow it generates back to shareholders in the form of dividends and stock buybacks.

The cash position more than supports strong dividend growth and payout in the future. Cisco has approximately 33% of its stock price in cash, or over $8 per share, and a low debt ratio of 29%, resulting in a net cash position of around $6 per share.

This offers Cisco plenty of room to keep up its commitments toward shareholders, even if business experiences temporary bumps in the road ahead, and provides investors with a large margin of safety in terms of future dividend growth and yield.

Cisco is diversifying and investing in growth

Cisco is not relying on its past glory and a pile of cash to generate future dividends. By combining dividend increases, stock buybacks, internal R&D and product launches with external acquisitions, the company has been using a very balanced mix of smart ways to enhance investor returns now, as well as secure stable and diversified earnings growth into the future.

Cisco has been on a shopping spree, transforming the company from a business dependent on tech hardware sales to a company that already has diversified technology income streams in various growing segments, and that still keeps diversifying and searching for growth.

I personally think that for such a large technology company, it is much smarter to carry out the growth strategy primarily through smart, selective acquisitions rather than trying to mimic the most innovative and most flexible startup companies in the world and attempting to invent all new products and services in-house. It would probably never see sustainable success with this strategy. A combination of in-house product launches and selective acquisitions of smaller companies with ready-made, freshly developed and marketed products is the right path to future growth for Cisco.

Stock valuation

Based on the current stock price of close to $25, the expected 5-year earnings growth of 8% annually, and using 10% as a discount rate, the Direct Cash Flow valuation method gives back an implied terminal rate of growth of 0% after the initial 5 years of 8% growth. I believe that the 8% growth rate is realistic, but the further growth of 0% is severely understated and the real growth will be higher. Even if it was just 2% per year, the company's estimated intrinsic value would be around $30. This represents an upside potential of approximately 20%.

Even if the initial growth is more muted, say, 5%, but lasted 10 years, with a 2% growth afterwards, the intrinsic value would still be $28.5, up 14% from today.

The risks

Acquisitions may not generate the same return on investment as Cisco's current business due to higher acquisition price or lower future sales growth and margins. Cisco mitigates this risk by buying at the most reasonable prices possible, as well as by using dividend payouts and stock buybacks to return at least 50% of the free cash flow it generates.

If Cisco's growth stopped immediately and never returned due to very adverse business conditions, its intrinsic value would drop to $18. This represents a 25% downside from the current price. However, even if such a situation occurred, Cisco has so much cash and could generate so much new free cash flow even at zero growth rate that it would be able to keep paying current dividends for more than a decade. At a lower share price of $18, the dividend yield would rise from 2.80% now to a very attractive stream of income of 3.7% annually.

Key takeaways

Cisco is performing the right steps toward future growth and capital appreciation, as well as current income generation for investors.

I am very bullish on Cisco for the long term. I recommend investors to slowly start building a position by dollar-cost-averaging and hoping for a pullback to make parts of the purchase at a better price. However, even at the current price, the company is not overvalued, but rather slightly undervalued; therefore, I am starting to buy now.

As a side note, I am not a technical trader, but a very long-term investor. But, if I was trading on technicals, my gut feeling would be to wait for a possible abrupt pullback after the next earnings release, if this earnings release disappoints or beats by a smaller-than-expected margin. However, I am not a short-term trader and based on my evaluation, Cisco stock is still an attractively priced dividend stock with excellent future earnings per share and dividend growth potential. Among tech stocks, I am also long on Microsoft (MSFT), which I recommended earlier this month, and I also described its costs of the monopoly.

提升卡

提升卡 置顶卡

置顶卡 沉默卡

沉默卡 喧嚣卡

喧嚣卡 变色卡

变色卡