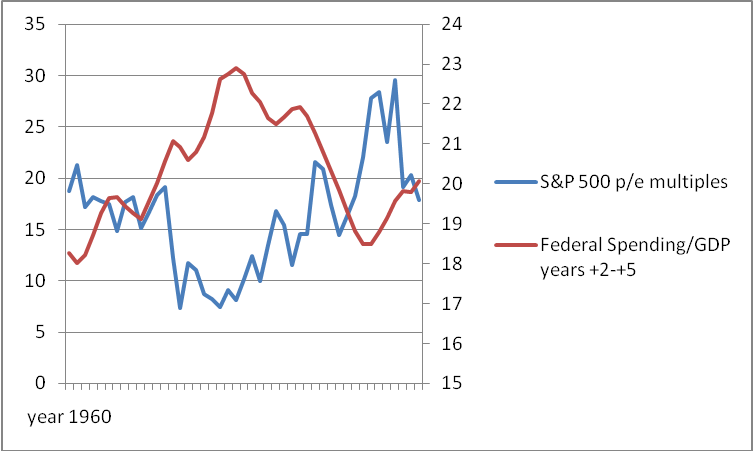

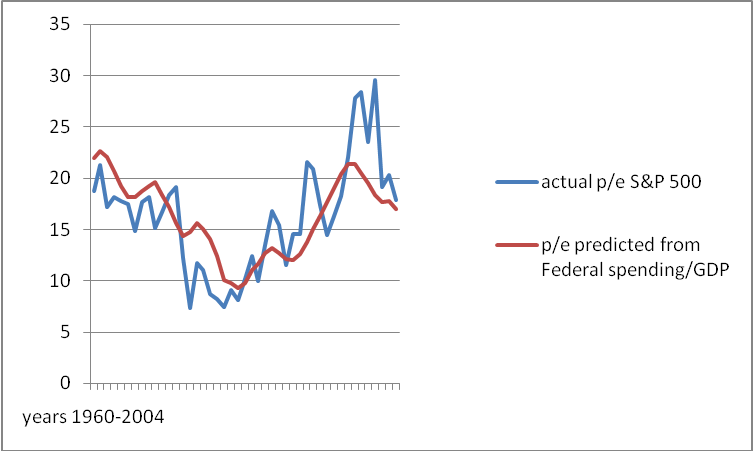

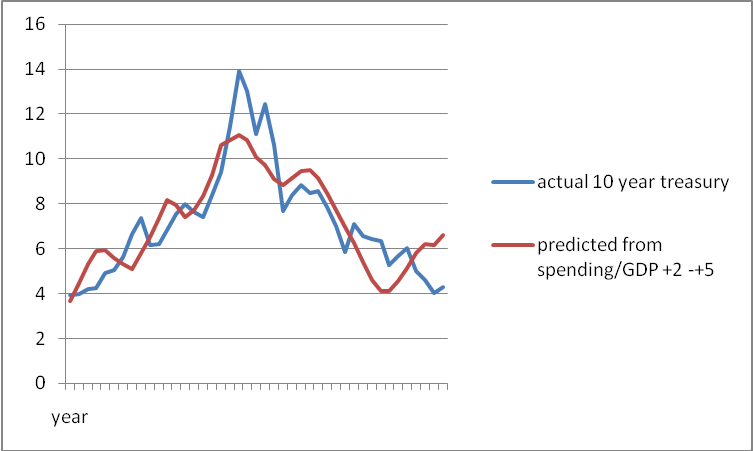

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.(More...) Any period's valuation of equities is determined by corporate profits and the multiple the market is willing to place on those profits. Macro economists typically take a top down approach to estimating profits. Determinants are typically GDP, labor cost, and inflation. Market strategists typically adopt a bottom up estimate of profits by aggregating views of industry analysts. A much less precise exercise is involved in determining the market multiple. Assumption of the multiple for any given year typically relate to the position of the market relative to the business cycle. Other inputs tend toward interest rate assumptions and the degree to which investors are under or overexposed to equities. In this note ,we take a more rigorous approach toward estimating the market's multiple. There is more than 50 years of data on the price to earnings multiple of the S&P 500. The S&P 500 is widely regarded as the best single gauge of the large capitalization U.S. equities market since the index was first published in 1957. The index includes 500 leading companies in leading industries of the U.S. economy, capturing 75% coverage of U.S. equities. Published data on the earnings of the S&P 500 are available from 1960 forward. In analyzing the market multiple we take cognizance of Milton Friedman's assertion that the best measure of the burden of government for any period is not the taxes it imposes but rather the amount that it spends. His logic was that government spending in one period must result in either taxes or borrowing, and that borrowing today means that taxes must be raised at some future date. One method of quantifying the extent that government spending impacts capital markets negatively is to examine the relationship between federal outlays as a percent of GDP and the price/earnings multiple of the S&P 500. It is generally accepted that the equity market acts as a discounting mechanism of expectations as market participants invest based on their perception of events and conditions to occur years into the future. This would suggest that the market multiple would be affected by the current as well as future levels of the ratio of outlays to GDP. We ran a series of regressions with the market multiple as the dependent variable and various averages of the current and future levels of the outlays ratio as the independent or explanatory variable. It should be noted here that using lagged values of the outlays ratio offered no statistically significant information. This suggests to us that indeed the equity market is a discounting mechanism, and that it is much more concerned with future levels of federal spending than with past levels. Forecasts of federal outlays relative to GDP are frequently published for many years into the future. These are performed twice yearly by the Office of Management and Budget in line with the Administration's budget proposals and updates. Currently actual data is available through fiscal 2009 i.e. October 2008 through September 2009, and forecasts extend through 2015 and even 2020. All estimates are in nominal dollars which is not problematic since the market multiple is based on nominal dollars. We experimented with various relationships between the multiple and the outlays ratio. In doing so our testing period extended with data from 1960 through 2004. This was necessary because we wanted to deploy actual data in our forward-looking indicator. The absolute best result was obtained using the average of the ratio in years 2 through 5 ahead of the current period's multiple. In other words the 2004 multiple is best explained by the average of the outlays ratio for the years 2006 through 2009. Not to confuse the issue, but because the ratio is based on fiscal year data the average is really 2005 through 2008 in calendar year terms. Chart I below shows a history of the raw data of the multiple and our look ahead ratio for the period under study. It shows clearly that the relationship is inverse meaning that higher multiples are consistent with a declining path of the outlays ratio. Chart II below shows the results of the regression fit between the two variables. The forward-looking outlays ratio explained 49.3% of the variation in the multiple with a highly significant "t" statistic of over 6. Given that there are many factors which should impact the market multiple, we found this result to be rather astounding. The causality that relates our expected outlays ratio to the market multiple is transmitted through the effect that the ratio has on interest rates. Higher interest rates cause required rates of return to increase and vice versa. Chart III below shows that 71.5% of the variability in Ten-Year Treasury rates is explained by our forward-looking outlays ratio. Of course the examination period is 1962 through 2004 so it excludes the anomalous 2008-2010 period. This stands out as an outlier because the economy has been in a liquidity trap. It also explains why the relation between interest rates, the outlays ratio, and the multiple broke down in the past two years. But Chart III also suggests that once the economy is out of the liquidity trap and conditions return to "normal" the expected outlays ratio will again dominate interest rates and the market multiple. Were interest rates to normalize to something akin to 5% on the Ten-year Treasury while the outlays variable also dropped, we could expect the multiple to expand. And of course were interest rates to stay low while the outlays ratio was projected to fall, one could expect a major expansion in the multiple. This outcome would be consistent with the views of the Austrian school of Von Hayek, Tea Partiers, and the Supply Side. The mantra is cut government spending and private sector growth will be unleashed so as to create enormous wealth and solve all the world's problems. An opposing view would be consistent with Keynes and the likes of Paul Krugman. The argument on this side would be that if government spending were reduced significantly, the outlays ratio would not fall as much as though because it would negatively impact GDP. Moreover, the reduction in output that would result would deflate the economy and kill corporate profits negating any positive impact on equity values from multiple expansion. This is the crux of the debate that has been occurring and we suspect that with the new Congress about to take control, it is a debate that will rage in the year ahead. Chart I - Historical Data - The Mkt. Multiple vs. Outlays Ratio (click to enlarge) Chart II - Regression for Mkt. Multiple vs. Outlays Ratio (click to enlarge) Chart III - Regression for Interest Rates vs. Outlays Ratio (click to enlarge) Additional disclosure: Please note that this article was written by Dr. Vincent J. Malanga and Dr. Lance Brofman with sponsorship by BEACH INVESTMENT COUNSEL, INC. and is used with the permission of both. |

狗仔卡

狗仔卡 发表于 2013-6-27 08:44 AM

发表于 2013-6-27 08:44 AM

提升卡

提升卡 置顶卡

置顶卡 沉默卡

沉默卡 喧嚣卡

喧嚣卡 变色卡

变色卡