|

|

楼主 |

发表于 2010-12-22 10:21 PM

|

显示全部楼层

回复 2# ppteam

Barrons Outlook 2011

While 2010 may have been a year of ambivalence and doubt–the Standard & Poor's 500 began January at 1115, then crisscrossed that line no fewer than 165 times as investors debated whether the government-engineered recovery will stick–it's ending with a clear consensus: 2011 should be a good year for stocks.

Collectively, the 10 strategists and investment managers surveyed by Barron's see the S&P 500 finishing next year near 1373, roughly 10% higher than Friday's close at 1244. But this solid if hardly extravagant target belies their increasingly expansive view of the U.S. stock market. A majority sees 2011 as the year when a sustainable economic recovery takes root, winning over skeptics and persuading both companies and consumers to relax their stranglehold on squirreled-away cash. Improving confidence and low interest rates bode well for corporate profits. Meanwhile, the Federal Reserve remains hell-bent on propping up asset prices, and wages and prices of goods aren't rising enough to sound an inflation alarm that would lead the central bank to alter its course of aggressive benevolence.

Against this backdrop, nine of the 10 strategists we polled are penciling in stock-market gains ranging from 7% to 17% for next year. That advance could be thwarted by escalating trade tensions; slowing global growth, as emerging economies tighten credit; and conflicts from Iran to the Korean peninsula. But the market has started to flinch less at each flare-up of risk.

Last spring, the escalating fiscal problems of southern Europe and Ireland triggered a broad flight from risky assets and a 15% pullback in U.S. stocks, but the second installment of European drama this November caused a mere 4% blip.

"THERE'S A GROWING SENSE that not every problem will be enough to topple the market," says Jeff Knight, head of Putnam Investments' global-asset allocation.

View Full Image

outlook_strats1

outlook_strats1

outlook_strats1

Maybe it's the passage of time from the 2008 financial crisis, and maybe it's the transfer of debt and risk from the private sector to the government, which, arguably, has more tools for managing disaster, but some of the feared perils have failed to materialize. The U.S. economy slowed at midyear, but didn't fall into a double-dip recession. Faster-growing countries from China to India began tightening credit, but haven't yet skidded to hard landings. And last week's extension of the Bush tax cuts, whether one agrees with them or not, means that our bailout tab won't have to paid just yet.

"None of the longer-term issues have been resolved: The developed world still has too much debt, wage growth is subpar, and central banks are running out of bullets to use during the next downturn," says Henry McVey, Morgan Stanley Investment Management's head of global macro and asset allocation. "But we're getting a cyclical reprieve, engineered by the central banks."

Nearly all the strategists expect stocks to outperform bonds, especially Treasuries. Even Douglas Cliggott, Credit Suisse's U.S. equity strategist, who sees the S&P 500 finishing next year almost flat—near 1250—says "You've really got to believe in outright deflation to put new money into bonds right now."

Others are even warier about bonds' prospects, with our government printing money liberally and interest rates already near historic lows. Since early November, even after the Fed detailed plans to pump $600 billion into the bond market, Treasuries have sold off violently enough to drive the yield on benchmark 10-year notes from 2.49% to 3.3%. "We've just started a secular bear market in bonds," says McVey, "and stocks are the proverbial best house in the neighborhood."

Admittedly, some of 2011's gains have been pulled forward. Stocks have rallied 19% since late August, when Fed Chairman Ben Bernanke & Co. first promised more monetary easing. Professional money managers seem quite fully invested in the short term, although that may not rule out further gains in the longer term.

It helps our consumer-driven economy that Americans are exhaling just a little. Nearly two years into our commitment to frugality, consumers have begun paying down loans, credit-card bills and other obligations with a little less urgency. Household debt has shriveled by $1 trillion recently, to $11.5 trillion. And the household-debt burden as a percentage of disposable income has eased, from 19% in 2007 to about 17%, near its 30-year average. Americans who once spent every penny now save nearly 6% of their disposable income, but the steady increase in savings has started to slow.

All these translate into more spending power–not by a lot, although it may feel like plenty after recent deprivation. We're not feeling flush, and our savings rate may never fall below a newly chaste 5%, but the slowing pace of consumer deleveraging is enough to prod the economy a bit and excite the market. In the third quarter, consumer spending grew 2.8%, the best rate since 2006, and retail, restaurant and recreation stocks levitated.

This spending uptick could have legs, if tight-fisted companies that have squeezed the most from productivity begin to hire anew. Most strategists expect the job market to thaw, if only because unemployment is already so high, at 9.8%.

"THE ECONOMY IS MOVING in a way that should cause confidence to improve, and that will affect everything from hiring to dividend payouts to consumer spending and equity-mutual-fund flows," says David Kelly, JPMorgan Funds' chief market strategist. Comments Barclays' U.S. equity strategist Barry Knapp: "We believe a bounce in business confidence is under way, and are seeing signs of increased business investment in capital and labor as a result."

Economic forecasters, of course, have a tendency to extrapolate today's conditions into the future, and, lately, the numbers are bright. Our factories are humming as manufacturing continues to expand, retail sales are rising, and optimism in even the beleaguered small-business sector has repaired to a three-year high. The private sector has added more than 1.1 million jobs in 11 months–hardly enough to replace the eight million-plus lost to the recession or to chisel away at our 10% unemployment rate, but enough to support some economic growth.

Investors aren't looking for much, anyway, and our strategists are forecasting growth of U.S. gross domestic product averaging just 3.2% next year. Since S&P 500 companies earn more than a third of their revenue abroad, and are especially hitched to commodity prices and business spending, "a V-shaped profit recovery can continue even without a V-shaped economic recovery," says David Bianco, BofA Merrill Lynch's chief U.S. equity strategist.

Companies Are Rich and Consumers Not So Poor

Corporations are hoarding a lot of cash, which, as the economy improves, could be put toward new hiring, or to buy back shares and pay dividends ...

... Americans are a long way from flush, but household debt and obligations have shrunk to levels closer to their three-decade average. As we have begun to exhale (a little), the increase in our savings rate also has started to slow.

[outlook chart 1]

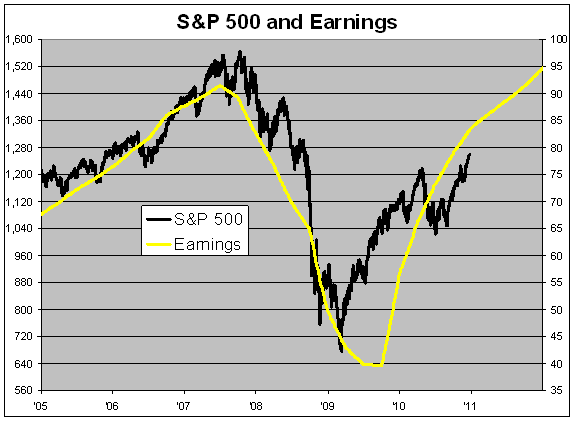

Cheap borrowing costs, brutal cost-cutting during the recession, and a lingering reluctance to hire during this uncertain recovery boosted profit margins and helped S&P companies earn a weighted average of $85 a share this year–up sharply from $61 in 2009. It wouldn't take much more growth next year to surpass the previous earnings peak of $88, hit in 2006.

And yet the S&P 500 fetches 13 times what companies are projected to earn next year—a price/earnings ratio that hardly seems stretched compared with the median multiple of 16 over the past decade. Clearly, investors question whether the recovery is sustainable, and don't see an easy way out of today's risible government spending. As debt shifts from the private sector to the government, so does the onus of deleveraging. Alas, our divided and distracted Congress doesn't seem to view deficit reduction as a pressing priority.

Meanwhile, Wall Street analysts expect S&P companies to earn roughly $95 next year, and Bianco thinks this frequently mocked target is within reach, even if our economy grows just 2%. For one thing, Merrill Lynch expects that provisions set aside by banks to cover loan losses will shrink from 2.6% in 2010 to 1.8% in 2011. Sales at S&P companies also grew 10% in 2010, thanks to foreign operations, business-to-business sales, exports and rebounding commodity prices, and Bianco sees revenue rising another 6% in 2011.

Nonfinancial companies also are sitting on record cash stashes, which make up 7.4% of corporate assets, the highest figure in five decades. These aren't earning much at the bank, and even after raising dividends to $30 a share in 2011 from $25 this year, and increasing expenditures by 10% to a projected $540 billion next year, S&P 500 companies will still be left with $480 billion in surplus free cash flow, Bianco estimates.

Corporate America learned a lesson during the credit crisis: Don't get caught having to raise money at the wrong time. That's why even cash-rich corporations like Coca-Cola (ticker: KO), Microsoft (MSFT), eBay (EBAY) and Wal-Mart Stores (WMT) have recently rushed to capitalize on the clamor for bonds by issuing debt at minuscule rates—all while they can. "Balance sheets and the ability to issue debt have never been stronger," Bianco says, "and I expect S&P companies to be major recyclers of fixed-income dollars."

That money stockpiled could be steered toward deals, hiring, research and development, or shareholder-friendlier moves.

Goldman Sachs strategist David Kostin expects buybacks to increase 25% to more than $340 billion in 2011, dividends to grow 11% to $270 billion, and companies to plow $240 billion in cash into mergers.

Kostin's 2011 target of 1450 for the S&P 500 makes him the most bullish in our survey, quite a change from his more guarded stance this summer. But improving economic data and forecasts prompted Goldman's economists to nudge up their 2011 U.S. forecast from 1.9% to 2.7%. Today, the cost of money has never been lower, U.S. inflation is low by most measures, and corporate-bond yields have never been lower, Kostin points out. Company balance sheets have never been stronger, and "the path of earnings growth has rarely been smoother."

WILL MAIN STREET SHARE Wall Street's enthusiasm? Stung by two recessions within less than 10 years and a "lost decade" of stock-market returns, many Americans are indifferent to equities. Since the current bull market began on March 9, 2009, the S&P 500 has climbed more than 83%. But during this stretch, investors have pulled nearly $111 billion from U.S. stock mutual funds and plowed more than $609 billion into fixed-income funds. Even those who don't think we're in a bond bubble must wonder if there's a bond-fund bubble.

Confidence Is Slowly Rising, Although Mutual-Fund Cash Is Running Low

Wavering consumer confidence seems to have bottomed and could improve if this government-goosed recovery proves sustainable. Even beleaguered small businesses, which are key to job growth, are starting to feel more optimistic.

But fund managers have been spending their cash. Wall Street needs Main Street to get excited about stocks for this run to continue.

[outlook chart 2]

Will things change in 2011? After the recent Treasury-bond selloff, fixed-income-fund investors receiving their fourth-quarter statements will feel pain for the first time in a long while, especially those convinced that they were moored in a safe harbor. And interest rates are likely to tick higher if the recovery sticks.

"Never in the history of investing has there been an orderly unwinding of the prior leading asset class," says Brian Belski, Oppenheimer's chief investment strategist, pointing to the messy selloffs of, for example, commodities and tech stocks after each peaked. "So why would it be orderly when bonds unwind?"

Lest anyone pegs Belski as a raging stock bull, his 2011 target of 1325 is among the more muted in this group. He was far more bullish in 2009, but has reined in his optimism as the bullish herd swells. He thinks that a secular bull market for stocks can arise –but only after the great unwinding of the bond market. Fortunately for stock investors, he notes, "much of the heavy lifting -- especially by Corporate America -- has already taken place, thanks in part to near-zero interest rates, two recessions, a re-employment cycle that is likely to emerge in the next several months and record high cash balances."

A year ago, the dozen strategists we surveyed had expected the S&P 500 to finish this year at 1239. That's almost a bull's eye, even if they didn't get all their reasoning right. For instance, they predicted, quite correctly, that the U.S. economy would grow slowly and erratically, despite lingering unemployment and plenty of scares along the way. But they also debated how our government would begin to wean our economy from the monetary life support. No one saw a second round of stimulus coming.

Strategists would much rather be contrarians, so the fact that those surveyed this year are in agreement with their peers makes some a little uneasy.

Adding to the anxiety: Our strategists aren't alone in their optimism: A mid-December survey of 302 global money managers showed more institutional investors flocking to bet on cyclical growth and commodity inflation. The horde expecting stronger global growth nearly tripled to 44% from just 15% in October—thank you, Ben Bernanke!—and those expecting better profits jumped to 51% from 11% two months ago.

Another red flag: Cash as a percentage of mutual fund assets—the available ammunition, so to speak—has recently fallen below 30%, and is approaching the depleted levels seen in 2000 and 2006-07. This shrinkage is partly due to the increasing values of stock and bond portfolios; and more than $2.8 trillion still sits in money-market funds. Yet it's also a clear sign that professional money managers are becoming more fully invested, at least in the short term.

But has this bullish consensus become pervasive and extreme? Even as stocks rallied this fall, ordinary investors were yanking money from domestic stock mutual funds and funneling it into bonds or emerging markets.

James Paulsen, Wells Capital Management's chief investment strategist, thinks that most investors still see risks everywhere. "Are people paying too much for houses? Are corporations overstaffed, and are banks lending too much? Look for broad acceptance of a sustainable recovery to take hold first" to signal that risk is rising, he says. Another cue: Wait for our central bank to tilt from policies aimed at easier money to those guarding against an overheating economy.

The lone strategist who doesn't see any upside for stocks in 2011 is Cliggott. The Credit Suisse strategist was surprised by this year's robust profit growth, but doubts it is sustainable.

"This profit cycle in the U.S. has been unusually dependent on the U.S. federal government borrowing enormous sums of money so that they could accelerate government spending and increase transfer payments to both individuals and to states, even as federal tax revenues fell sharply," he argues. "But it's hard to imagine the federal government will keep spending $1.60 for each $1 in tax revenue."

At some point, government spending will need to be cut and taxes raised, which will slow economic and profit growth. "Perhaps it will be a story line in 2012, or 2013–time will tell," notes Cliggott, who expects profit margins to peak in mid-2011.

INFLATION MAY ALSO THICKEN the plot by that time. Loose money policy has already driven crude oil to a two-year peak, and copper last week reached an all-time high. The consumer-price index in the U.S. has risen just 1.1% over the past year, but prices have increased 5.1% in China. When inflation in China–now the world's most-watched growth engine–rises enough to require government restraint to cool off, then watch out.

Michael Ryan, UBS Wealth Management's chief investment strategist, thinks that profits could grow more than expected as corporate cash-hoarding ends, the pace of consumer deleveraging slows, and housing becomes less of a drag on the economy. But he expects geopolitical threats to intensify, and sees the sovereign-debt crisis growing more acute as weak links in the European Union are tested. Next up: Spain, where the cost of insuring against defaults is rising and whose credit rating might get downgraded by Moody's.

"Given Spain's relative importance in the euro zone and Germany's reluctance to underwrite any additional rescue packages, the crisis will shift from concerns over liquidity to fears of solvency," Ryan notes. On this side of the Atlantic, municipalities weakened by declining tax revenues, overextended public services and underfunded pension plans will struggle. "What remains to be seen is whether we'll see a default by a high-profile city big enough to change risk perception," he says.

The Year That Was

View Full Image

outlook timelin

Illustrations: Bobert Neubecker for Barron's; Photographs (left to right): Ed Lallo/Bloomberg News; Kostas Tsironis/Bloomberg; Jewel Samad/AFP/Getty Images

outlook timelin

outlook timelin

Ryan also doubts that the housing market will bounce back, given the 8.6 months it would take to exhaust the backlog of unsold homes, a still-high level of foreclosures and the prevalence of negative housing equity. UBS sees the S&P Case-Shiller home-price index slipping 5% in 2011. But because housing is already depressed, and "price declines are likely to be manageable, continued weakness in residential real estate won't trigger another recession," he predicts.

Morgan Stanley's McVey thinks housing is "the swing factor of economic variables," and interest rates must rise in an orderly fashion for the stock market's valuation multiples to hold. Unless housing is fixed, the S&P 500's profit growth could turn negative by mid-2012. And ultimately, "the Fed and the government have to engineer job and wage growth," he says. "If they don't, the equities-over-bonds trade is just that–a trade."

So where should we invest? Belski sees dividend investing as the bridge from bonds back to equities, and suggests looking for companies best poised to raise payouts.

He screened for S&P 1500 companies with strong free cash flow, a history of dividend hikes in each of the past 10 years, a credit rating of A-minus or better from S&P and a dividend yield comparable to 10-year Treasuries. His list of 18 includes Abbott Laboratories (ABT), Automatic Data Processing (ADP), Bemis (BMS), Genuine Parts (GPC), Illinois Tool Works (ITW), Pitney Bowes (PBI) and apparel-maker VF (VFC).

Goldman's Kostin tracked down 25 heavy-lifters that account for two-thirds of the S&P 500's projected margin growth next year. Ten of these are tech companies, and his list includes Apple (AAPL), Google (GOOG), Oracle (ORCL), Qualcomm (QCOM), ExxonMobil (XOM), Merck (MRK) and Pfizer (PFE).

On the other hand, Kostin also screened for stocks whose projected 2011 margins are uncomfortably high relative to their historical margin peaks. These carry the loftiest expectations—engineering firm Cummins' 2011 margins (CMI), for instance, are 130% that of its previous peak. Others on that list include Cliffs Natural Resources (CLF), MedcoHealth Solutions (MHS), VeriSign (VRSN), Hospira (HSP) and Ford (F).

Putnam's Knight thinks that the starkly divergent policies between countries like China and Brazil that are tightening monetary policy and the U.S. will manifest itself most directly in the currency markets. Diversified portfolios ought to have exposure to the strengthening currencies of the emerging markets as well as Australia, Canada and Scandinavia, he says.

Given their bullish bent heading into 2011, many strategists are tilting toward cyclical sectors that historically thrive as the economy improves. "The noise of the spring and summer only pushed out the recovery," says Belski, "moving the cycle back a few steps only to see fundamentals reignite the cycle again in the fall." His advice: Focus on areas likely to grow with the economy, such as technology, industrials and consumer discretionary.

SOME THOUGHTS on the strategists' sector selection:

• Technology is favored by eight of our strategists and shunned by none. The beloved sector can seem sexy and safe at the same time -- it's hitched to business spending and global growth, holds the allure of improved productivity for cost-conscious employers, and is backed by the deepest pockets. But is it becoming a crowded trade? Many individual investors burnt by the tech bubble are still wary, but when they start coming around, be careful.

• The new pariahs are utilities and health care, which between them amassed 12 disses and just one nod. Contrast these with energy and industrials, each favored by five strategists and avoided by none. The case against rate-sensitive utilities is well understood, and the threat of rising interest rates quite real. But at some point, the collective lunge at growth will get old, and cheap-enough stocks will start attracting attention.

• Given the uncertain pace of the housing-market recovery, banks' exposure to sovereign debt problems, and the fragile state of consumer confidence, most strategists are neutral on the financial and consumer-discretionary sectors. The few who weighed in are split.

Investors Buy Into Economic Recovery

Consumer discretionary and industrial shares topped all other sectors in the S&P 500 as utilities and health care fell out of favor.

Sector 2010* 2009 2008 2007

Energy 13.5% 11.3% -35.9% 32.4%

Materials 14.9 45.2 -47.1 20.0

Industrials 21.8 17.3 -41.5 9.8

Consumer Disc 24.3 38.8 -34.7 -14.3

Consumer Staples 10.0 11.2 -17.7 11.6

Health Care 0.4 17.1 -24.5 5.4

Financials 7.2 14.8 -57.0 -20.8

Info Technology 8.4 59.9 -43.7 15.5

Telecom Services 10.4 2.6 -33.6 8.5

Utilities -1.0 6.8 -31.6 15.8

S&P 500 10.8 23.5 -38.5 3.5

*As of 12/15/2010. Source: Standard & Poor's

Consumer-discretionary stocks, a group that includes Nike (NKE) and Priceline.com (PCLN), have rallied 24% this year and are 2010's top performers by far. It's widely—and perhaps correctly—assumed that demand might stay sluggish. What is underappreciated, however, is how rapidly companies are restructuring their supply chains. The competition, those left standing after the credit crunch, also is more rational. In light of these factors, and with so many fence-sitters, a slight improvement in demand could go a long way.

• Consumer staples gained 10% this year, and have gotten a little lost in the latest growth scrum. Raw-material costs are rising, but many of these companies have strong balance sheets. They have an appealing average dividend yield of 2.7%, and rake in enough cash flow to maintain and raise their payouts.

Many of the companies in this group, such as PepsiCo (PEP) and Procter & Gamble (PG), get much of their revenue and profits from fast-growing emerging markets. Says UBS's Ryan: The sector doesn't just have a global footprint, but it has the right one. And that could pay off nicely in 2011. |

|

狗仔卡

狗仔卡 发表于 2010-12-22 10:16 PM

发表于 2010-12-22 10:16 PM

提升卡

提升卡 置顶卡

置顶卡 沉默卡

沉默卡 喧嚣卡

喧嚣卡 变色卡

变色卡 发表于 2010-12-23 04:59 AM

发表于 2010-12-23 04:59 AM

谢谢

谢谢