Really.

Last night one of the wonderful forum folks dug up a post from another blog

who had in turn dug up a published Fed document that settled in no

uncertain terms the entire "hyperinflation/deflation" debate.

Simply put, this debate is over.

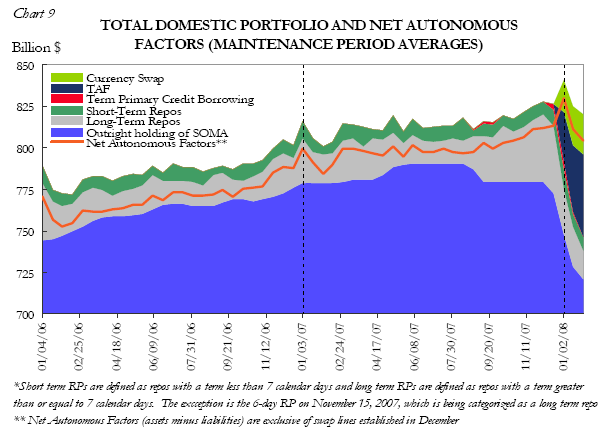

The

Fed has been aggressively draining the SOMA account, with the pace of

that drainage stepping up precipitously since December.

Draining.

Not adding.

The whole report (in PDF format) can also be accessed.....

The "money graph" is right here:

Why?

You

can think of the SOMA as the Primary Dealers (big banks) "margin"

account. (This is not strictly accurate, but is close enough.)

Many market crooners and "technicians" have been stating that "The Fed is hyperinflating to bail out the economy."

The facts say otherwise.

This has profound investment implications.

- If you are investing today on the premise that "The Fed has our backs", you're wrong.

- If

you are buying metals in the belief that The Fed is intentionally

devaluing the dollar and hyperinflating the money supply, you're wrong.

- If you think The Fed is intentionally being "the bagholder of last resort", monetizing bad debt, you're wrong.

- If you think The Fed leads the market and sets rates, again, you're wrong. (Read the entire PDF - very carefully - you will find that The Fed is in fact following the market, and admits so!)

There simply is no more debate on any of these points, because we now have the actual data from the Horse's Mouth.

There are is no more "postulating" this or that, as we now have the facts, and they are what they are.

- There is no bailout in process via monetization. Period.

- There is no hyperinflation via "printing." Period.

- The Fed does not "set" interest rates. The market does, and The Fed then does their damndest to deal with it. Period.

In fact, The Fed is actually taking down risk,

as I have said repeatedly, and de-leveraging not only their own balance

sheets but they are also forcibly taking down risk in the primary

dealers - whether they like it or not!

Now we know - for a fact

- why Citibank had to go to the Arabs for money at double-digit rates.

Why the other money-center banks are issuing preferreds and other

instruments with returns at more than double the interest coupon

required to borrow through the primary Fed credit facility (whether it

be the TAF or the Discount Window.)

We now know the facts of life:

- Fact: The good collateral has all been pledged.

- Fact: The margin credit supply has been decreased.

- Fact: Risk capacity is being withdrawn actively by The Fed.

- Fact: The money supply is deflating.

Get that all in your head and make sure it sticks, because if it is not the foundation of your investment thesis over the next several months, you are proceeding from an incorrect premise.

Oh, and there are others who can read too, despite the nutjob-grams I've received in my email since posting this originally. Try this one on for size:

"Fear

that a hobbled banking sector may set off another Great Depression

could force the U.S. government and Federal Reserve to take the

unprecedented step of buying a broad range of assets, including stocks,

according to one of the most bearish market analysts.

That extreme scenario, which would aim to stave off deflation and stabilize the economy, is evolving as the base case for Bernard Connolly, global strategist at Banque AIG in London." The base case?!

You mean to tell me that this is not an outlier any more; this is actually what we have professional analysts EXPECTING to happen?

Gee, its not just "nutjob bloggers" who can read any more, eh?

There is plenty of other news, but that's something for another time - and another ticker.

Recalibrate your thesis folks.

We are no longer dealing with postulates and hypotheses.

We are now dealing with facts. |

狗仔卡

狗仔卡 发表于 2008-9-28 08:05 AM

发表于 2008-9-28 08:05 AM

提升卡

提升卡 置顶卡

置顶卡 沉默卡

沉默卡 喧嚣卡

喧嚣卡 变色卡

变色卡 发表于 2008-9-28 11:28 AM

发表于 2008-9-28 11:28 AM