|

|

发表于 2009-11-22 03:09 PM

|

显示全部楼层

发表于 2009-11-22 03:09 PM

|

显示全部楼层

本帖最后由 yaobooyao 于 2009-11-22 15:11 编辑

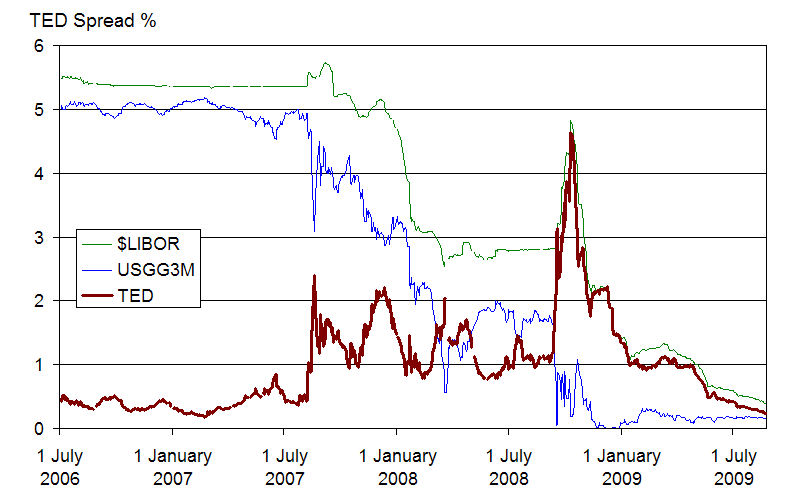

TED Spread widening, 也许是因为Year End Window Dressing driven, 因为Pure Cash on Balance Sheet is not good looking, so the purchase of short term T-Bills is just a face-lifting effort (把cash 换成30~60天的T-Bill, 就变成了short term investment asset, 但其实它的真实回报率是低于0.25% 的FED Rate 的, 因为抢购T-Bill 的机构太多了) with no economic value (as the annualized real return rate on this T-Bill is less than FED rate, which is the 'negative return' comes from).

I see the LIBOR rate is still quite stable (Eurodollar 的利率基准), the TED Spread looks like purely T-Bill's move by itself. Unless there is a spike on LIBOR and at the same time a diminishing marginal return on T-Bill, that will spell panic in credit market again.

Just my 2 cents. |

|

狗仔卡

狗仔卡 发表于 2009-11-22 02:54 PM

发表于 2009-11-22 02:54 PM

提升卡

提升卡 置顶卡

置顶卡 沉默卡

沉默卡 喧嚣卡

喧嚣卡 变色卡

变色卡